If you spend any time in Chicago investor circles, you hear the same phrases over and over. Sheriff sale deals. Bank-owned steals. Off-market distress. The story usually sounds like this. Someone bought a foreclosure in Cook County for a fraction of its value and turned it into instant equity or steady cash flow.

You do not hear as many stories about the investors who rushed in without doing their homework and found out later that the property came with tax surprises, angry tenants protected by local law, or a demolition order from the city.

Buying foreclosure and distressed real estate in Cook County can be smart. I work with investors who have built entire portfolios on those opportunities. The difference between a great story and a horror story is not luck. It is preparation.

In this article, I am going to walk you through how buying distressed and foreclosed properties really works in our office at The Bow Tie Attorney. We will talk about judicial sales, REO and bank-owned deals, and off-market distress, and we will focus on the legal homework smart investors do before bidding. If you are searching for “how to buy foreclosures in Chicago” or “Cook County sheriff sale investing,” my goal is simple. I want you to know what to look at before you raise your hand or send a wire.

If you are looking at a Cook County foreclosure or distressed property, The Bow Tie Attorney can review the legal side of the deal so you know what you are really buying before you bid.

When investors talk about buying “foreclosures” in Chicago, they are usually talking about one of three paths. Each one has its own rules and its own risk profile.

Each path can produce good deals. Each path can also produce expensive headaches if you treat it like a simple spread between list price and after repair value.

When investors hire me to help with distressed acquisitions, the first question I ask is not “What is the ARV.” It is “Which path are we on and how much control do you really have in this process.” That answer tells us what information is available, what deadlines apply, and how much room we have to negotiate if we find something ugly hiding in the file.

At a Cook County judicial sale, you are not just buying a house. You are buying whatever interest the court is allowing to be sold under the foreclosure judgment. That usually means the mortgage holder’s interest and everything junior to it that was properly named, served, and cut off in the case.

Smart bidders do not just read the sale notice. They review the court file. Before you ever show up at a foreclosure auction in Cook County, you want to know:

In our office, a judicial sale pre bid review often starts with a quick but disciplined docket check and a targeted look at the judgment and orders. The goal is to spot reasons a deal might collapse after you are already the winning bidder, when backing out becomes expensive or impossible.

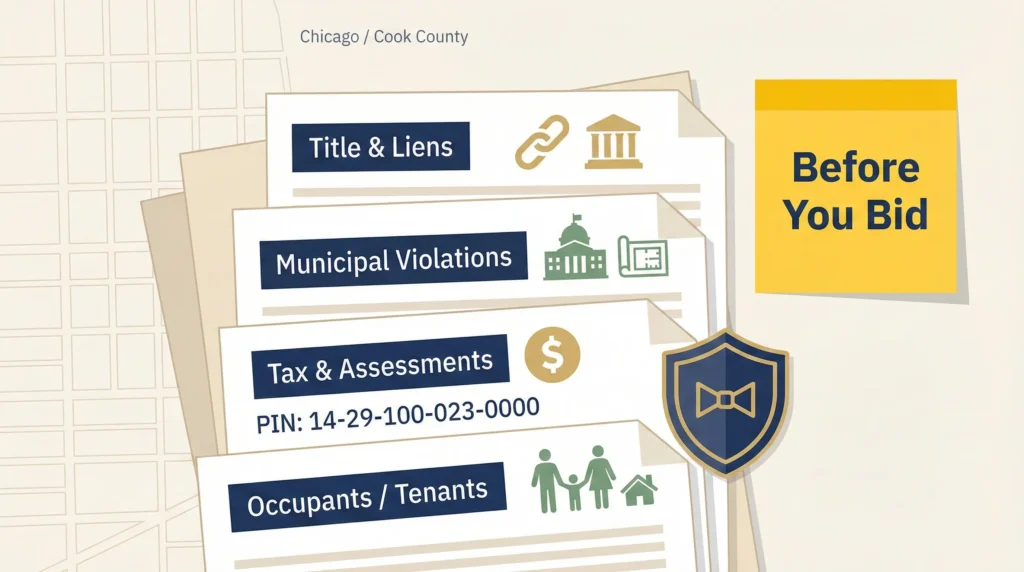

Every distressed property has a story. Title tells a big part of it. Municipal records tell another. If you skip either, you are guessing.

Before my investor clients put serious money at risk, we look at:

One of the most painful calls I get is from an investor who just took title to a distressed property and then discovered a long running code case with steep daily fines or a looming demolition order. That information is often discoverable before you buy. The question is whether anyone bothered to look.

On a spreadsheet, a distressed acquisition is simple. Closing date in, renovation timeline, rent or resale timeline out. In real life, one of the biggest variables is who lives in the property and what rights they have.

In Cook County, you may be dealing with:

Before my investor clients bid on a property, we talk about the occupant picture as clearly as we can. That includes reviewing any rent rolls we can obtain, checking for recorded leases or notices, and looking at the foreclosure file for references to tenants. We also talk about the local rules that will shape your exit strategy, including Chicago’s Residential Landlord and Tenant Ordinance and relocation requirements in certain situations.

Buying distressed real estate without a plan for who is inside is one of the fastest ways to turn a good deal into months of stress and unplanned expense.

Before you buy in tenants, code issues, or unknown liens, The Bow Tie Attorney can help you build a clear picture of the people and problems attached to a distressed Cook County property.

Many Chicago investors prefer REO and bank owned properties to courthouse steps bidding. You get access, you get an MLS listing, and you often get more time to close. That does not make these properties simple.

When you buy an REO, you are usually signing the bank’s paperwork, not your own. That paperwork often includes:

Part of my job in REO deals is to translate those documents into plain English and help investors decide whether the risk fits the price and their business plan. Sometimes that means negotiating tweaks. Sometimes it means walking away from a property that looks good on the flyer but bad on paper.

Some of the best distressed opportunities never reach the sheriff’s sale or the REO list. They are created when investors work directly with owners in trouble, heirs who have inherited a problem, or note holders who want out.

In those files, legal homework looks a little different. We may be:

These deals can be win win when handled correctly. You help someone exit a bad situation. You acquire a property with more access and more control than a courthouse auction would give you. The key is respecting the foreclosure process and the people involved instead of trying to sneak around them.

If you want to buy distressed and foreclosed property in Cook County without betting your portfolio on guesswork, a strategy session with The Bow Tie Attorney can help you build a legal due diligence checklist that fits how you invest.

At a sheriff’s sale you are bidding at a court ordered foreclosure auction, usually with limited inspection rights and no traditional contingencies. You buy the interest being sold under the judgment, subject to any liens or issues that survive the foreclosure. In a regular retail purchase, you have contract contingencies, inspections, and more negotiation power around repairs, title issues, and closing terms. The upside at a sale can be greater, but so can the risk if you do not research the case and the property.

Often yes, but the availability and scope of title insurance depend on the path of the deal and the specific issues in the file. Many REO and post confirmation purchases involve title policies with certain exceptions. Sheriff sale purchasers can sometimes obtain title insurance after the sale and confirmation, but title companies may require additional documentation or exclude known risks. This is one reason we like to review preliminary title information before clients commit serious money to a distressed acquisition.

When interior access is not available, you focus on what you can see and what you can read. That includes exterior drive by inspections, public records, code and violation searches, tax history, foreclosure file review, and talking to neighbors when that is appropriate. You also adjust your numbers to reflect the fact that you are buying a mystery box. Smart investors build in larger repair buffers and reserve higher risk deals for only a portion of their portfolio.

It depends on where you step into the process and who is in the property. If you buy at sheriff’s sale, there is usually a delay for confirmation of sale and any possession orders or stays. If you buy from a bank as an REO, you may receive a deed with occupants still inside and need to follow local eviction and relocation rules. In off market distress, you might negotiate a move out schedule with the seller in the contract. In every case, it is important to understand the legal steps for obtaining possession rather than assuming you can change locks immediately.

Legally, you may not be required to have a lawyer at every stage, but practically, most serious investors use one. The money you save by avoiding one bad deal or by structuring one complex deal correctly can easily cover the cost of legal advice. My job is not to talk you out of every risk. It is to help you see the risk clearly and decide whether it fits your strategy and your tolerance.

Most investor relationships start with a simple conversation. You tell me how you like to buy, what types of Cook County properties interest you, and where you have felt exposed in past deals. From there, we build a pre bid and pre contract checklist that fits your style. On live deals, you send over the sale notice, basic property information, and any available documents. We review them, flag the legal issues, and help you decide how aggressive your offer or bid should be.

Stay ahead of industry changes with our comprehensive continuing education program. New courses added monthly, covering everything from legal updates to market trends.

Connect with like-minded professionals who share your commitment to excellence. Build relationships that last beyond any single transaction or market cycle.

Position yourself as the go-to expert in your market. Our advanced certifications and specializations help you stand out in an increasingly competitive landscape.

“Excellence is not a skill, it’s an attitude. In real estate, that attitude translates to meticulous preparation, unwavering ethics, and an uncompromising commitment to client success.”

— Mahmoud Faisal Elkhatib, The Bow Tie Attorney